Investor notes from the fields of the Neural Interfaces Summit 2023: medtech and consumer

Neural interface technologies (neurotech), defined as ‘...devices that interact with the nervous system of an individual’, have taken centre stage at the recent JP Morgan Healthcare conference. It's remarkable that neurotech companies have raked in hundreds of millions in sales and carried out thousands of procedures annually. One notable player in this field is Neuronetics. This public company has delivered nearly five million treatment sessions to thousands of patients with major depressive disorders using transcranial magnetic stimulation (TMS). However, despite these impressive statistics, it's important to note that the field is still in its infancy, both in terms of funding and patient numbers.

Investment landscape

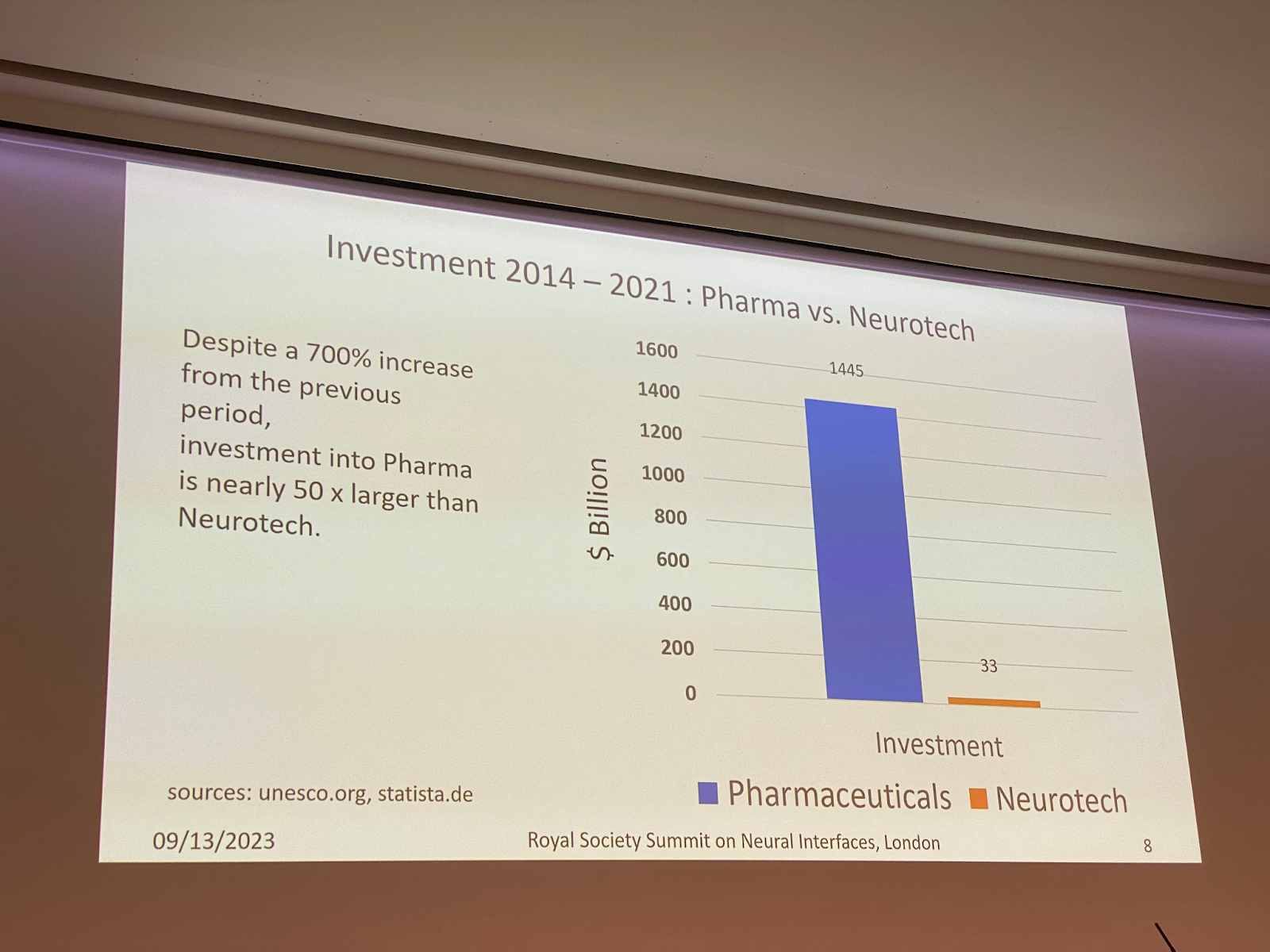

Jörn Rickert, the CEO and a co-founder of CorTec and Neudo, points out that investments in pharma are a whopping 50 times larger than investments in neurotech [1]. My more pessimistic estimates suggest that about $5 billion has been invested in 178 neurotech startups, with Neuralink alone receiving $638 million, accounting for approximately 13% of the total investments.

Chart 1. Investments in Pharma vs. Neurotech, 2014-2021 [1]

Tech landscape

Deep brain stimulation (DBS), a well-researched and adopted invasive neurotechnology, has been used to treat approximately 250,000 patients since its inception [2]. Regarding patient numbers, DBS is probably second only to cochlear implants, which have been used to treat around 400,000 patients [7]. However, the annual number of DBS treatments remains relatively low, with only about 25,000 patients receiving treatment. In Europe, the number of people who actually undergo treatment is a mere 3% of eligible patients [2]. The hesitancy among patients can be attributed to concerns about potential side effects, the economic burden (with an average cost of $30,000 per patient), alternative treatment options, disruptions to social routines, and other factors.

The field of DBS continues to advance. Recent advancements include better imaging techniques (such as anatomical and functional imaging from 3T to 7T), operations performed under general anaesthesia, intraoperative MRI for placement verification, remote access and programming of DBS, rechargeable battery technology, smaller systems, and directional stimulation [2]. These advancements contribute to the expanding application domain of DBS, offering hope for more patients and potential cost reductions due to economies of scale.

DBS has already been applied to more than 50 clinical disorders, with approximately 71% of them being movement disorders and 16% in the realm of psychiatry. The remaining clinical applications include epilepsy, cognitive disorders, pain management, and other conditions. Currently, 35 ongoing clinical trials explore future DBS indications [2].

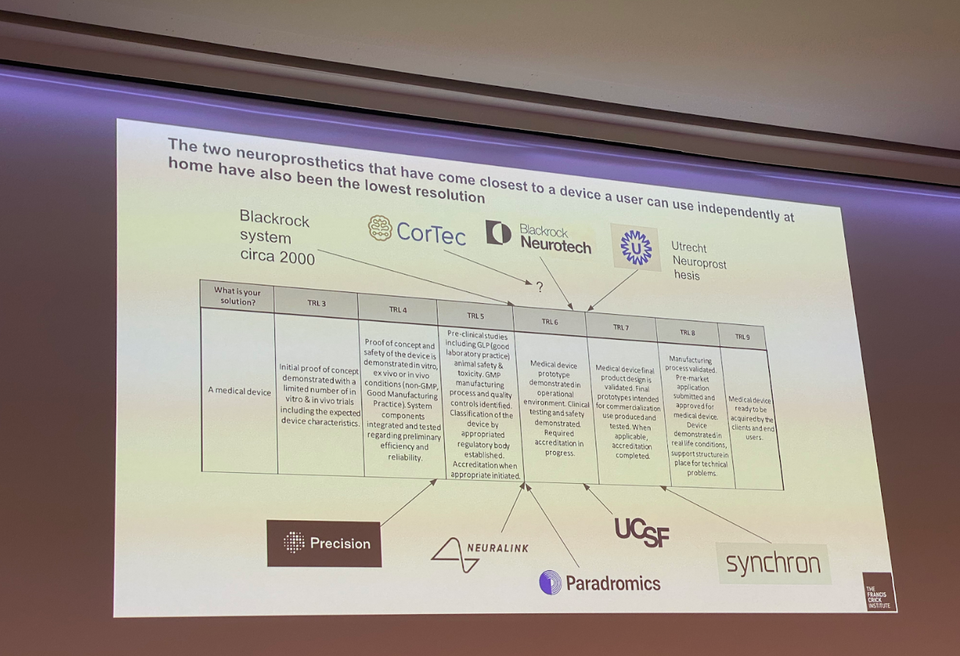

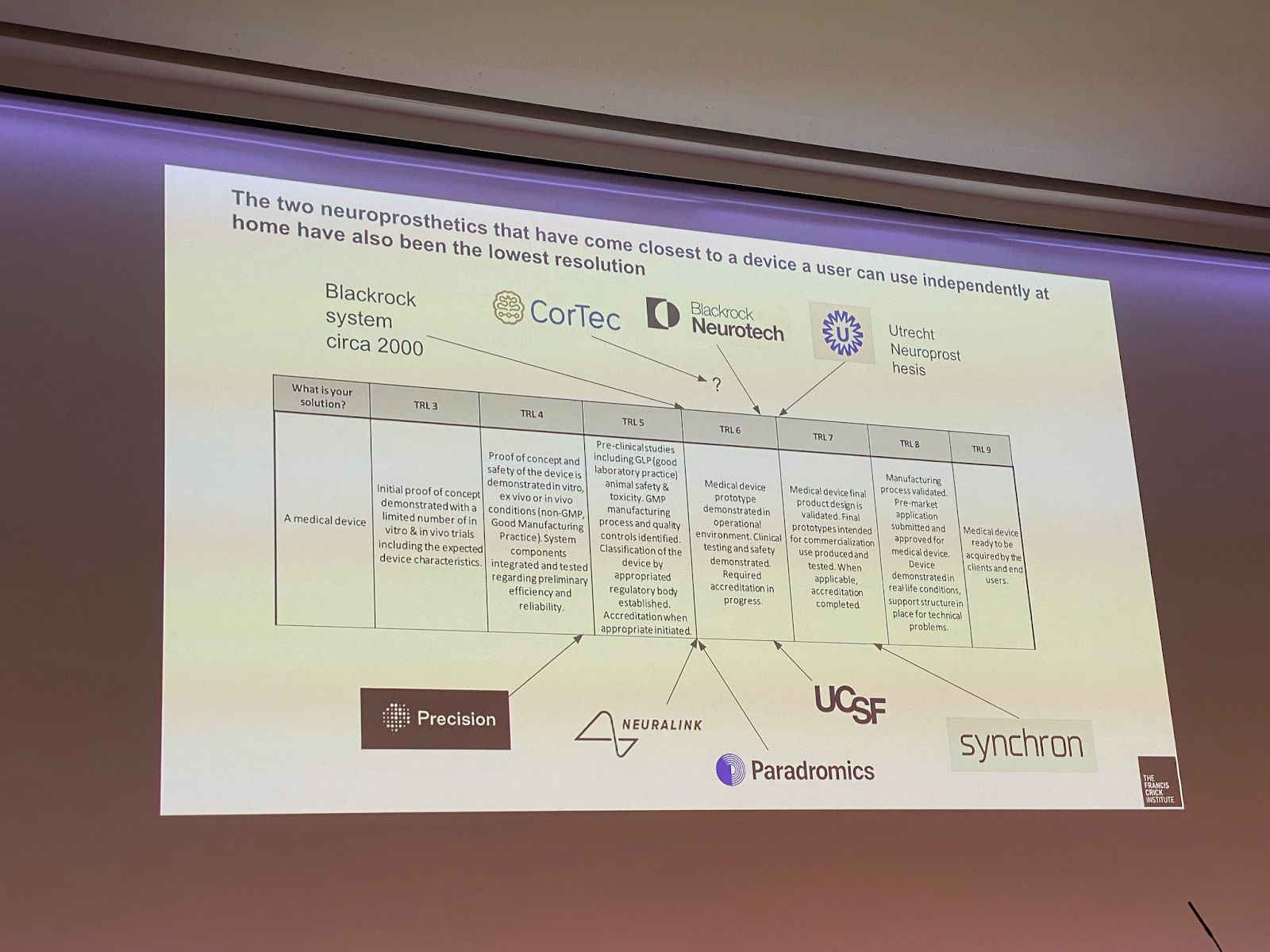

While DBS is a well-established technology in the neurotech world, other invasive modalities are further behind in terms of clinical deployment. For instance, Blackrock Neurotech's microelectrode array and Synchron's endovascular electrode array are currently at technology readiness levels six and seven, respectively, out of a total of nine levels (chart 2). These systems have already been demonstrated in operational environments, undergone clinical and safety testing, and are now on the verge of final prototype validation [3].

Chart 2. Selected neurotechnologies commercialisation stage [3]

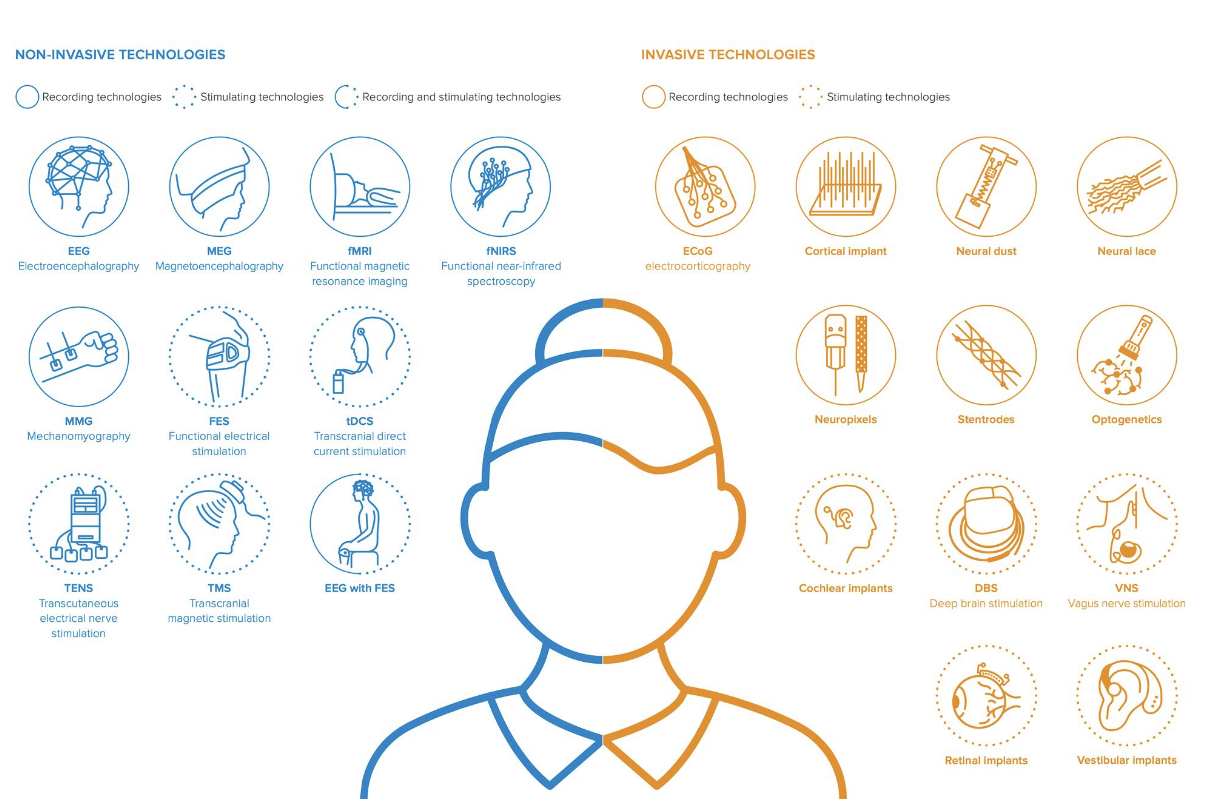

In addition to invasive systems, non-invasive or less invasive neurotech systems are also developing. A report released by The Royal Society in 2019 listed ten non-invasive technologies (such as EEG, MEG, and fNIRS) and twelve invasive technologies (including ECoG, cortical implants, and stentrodes, mentioned earlier) that make up the neurotech field (Chart 3).

Chart 3. Invasive and non-invasive neurotechnologies [The Royal Society]

The progress made in non-invasive neurotech is truly astounding [4]. Developments in transcranial magnetic stimulation (TMS) and transcranial ultrasound stimulation (TUS) have been particularly remarkable. These include the introduction of repetitive and closed-loop TMS, the development of curved transducers for targeting specific brain regions with TUS, and the advancement of sophisticated transducers with as many as 256 elements to reach deeper areas of the brain, such as the lateral geniculate nucleus.

While much of the focus at the summit has been on directly connecting to the brain, there have also been significant advancements in technologies targeting nerves. For example, transcutaneous auricular vagal nerve branch stimulation, in the form of an earphone-like device, has gained widespread adoption since 2019. Other developments include the use of neurovascular bundle cuffs, thin-film helical cuffs, and thin-film multichannel cuffs, which supplement long lead pacemaker-style stimulators of the vagal nerve [5].

Clinical translation, wider adoption, platformisation

As the neurotech toolkit continues to expand and improve, the challenge lies in successfully integrating these technologies into clinical practice and building multi-billion-dollar companies around them. As Will Muirhead concluded in the presentation, ‘human high-resolution neural recording is here - we need to work out how to use it for patient benefit’ [3].

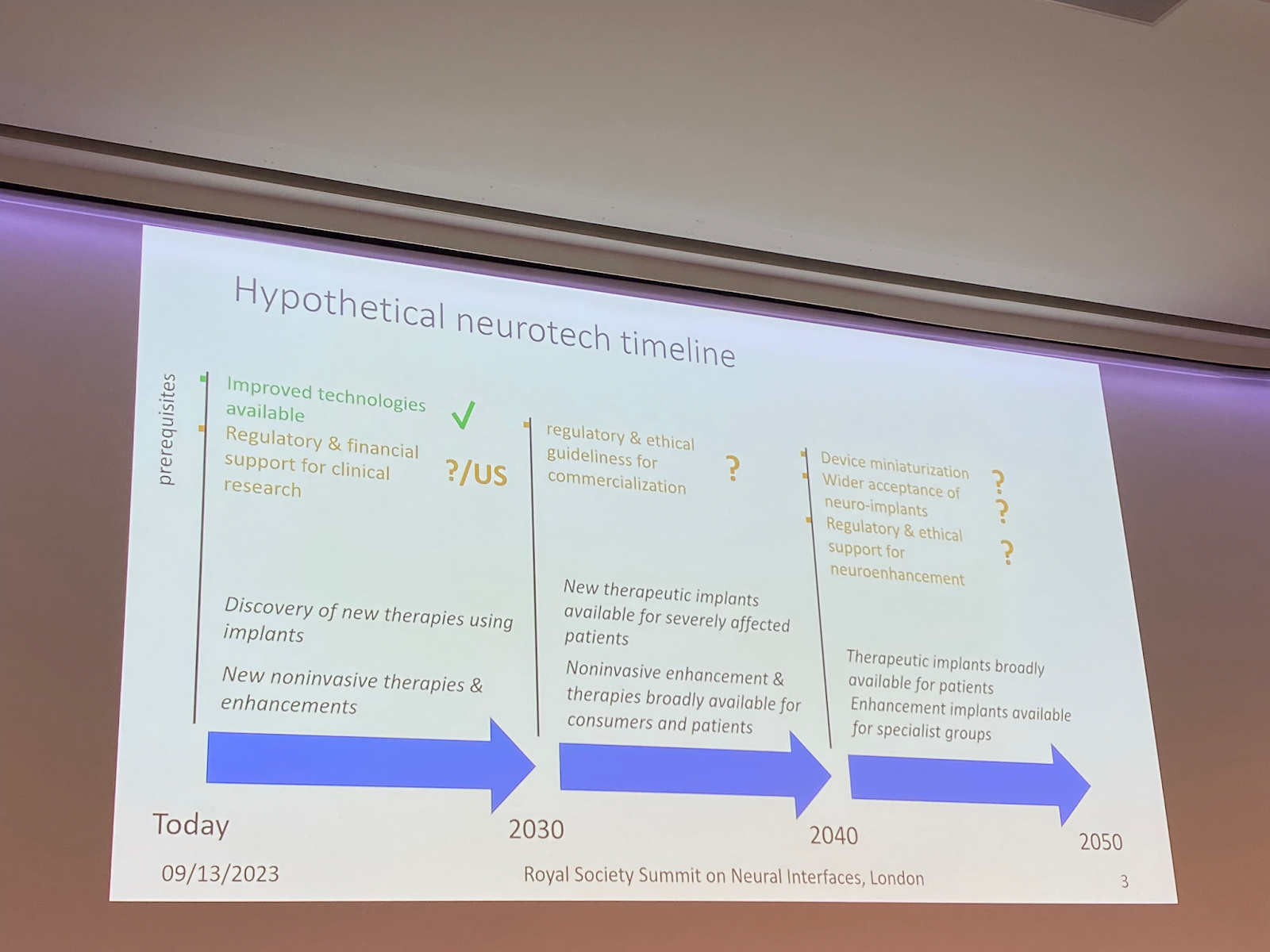

Another challenge is expanding neurotech to consumer markets. Jörn Rickert believes that neurotech is at the stage where ‘improved technologies are available’. However, we are decades away from ‘therapeutic implants [being] broadly available for patients [and] enhancement implants available for special groups’. Rickert predicts that the 2050es may be the turning point when therapeutic implants and limited enhancement implants become more accessible (Chart 4) [1].

Chart 4. Neurotech adoption timeline [1]

The slow expansion of neurotech from healthcare applications to enhancement use cases and consumer markets can be attributed to various factors. One such factor is the distinct demands and technological requirements of these markets, along with the initial appeal of the healthcare sector. While patients prioritise restoring lost functions, at least to some extent, consumers seek devices that can elevate their performance beyond what an average healthy individual is capable of.

Tim Danisson noticed that ‘patients' priorities do not align with cool demos we build…[and] it’s not just about [high] resolution [neural recording].’ He then explained that a cochlear implant with 20 channels almost lets a patient hear words and sentences. However, a much simpler version with just one channel is also beneficial, as it helps a patient read lips better [6].

It makes sense for entrepreneurs to zero in on medical devices that, though limited in scope, deliver critical and highly sought-after functionalities. At the same time, this approach marks a departure from the broader consumer tech industry's mantra of packing devices with an arsenal of features, aiming to outdo competitors and future-proof products for yet-imagined applications.

Building systems that can expand from precision to excess in terms of functionality, for example, via modularity, will allow neurotech to align with the consumer tech world. Modularity was also mentioned in the context of neurotech inclusivity by Conor Russomanno, the CEO of OpenBCI, a company that develops devices in various form-factors, allowing for types of sensors [8].

Sometimes, repurposing a medical device for consumers by expanding its features is impossible, as the underlying technology may not fit the market. Look at a popular idea of brain-computer interface. Denison mentions, ‘BCI folks are excited about cortex, but therapies are subcortical’. However, there are some encouraging signs that medical and consumer neurotech will overlap, as more non-invasive modalities are emerging and underlying enabling technologies are being developed to reduce device costs.

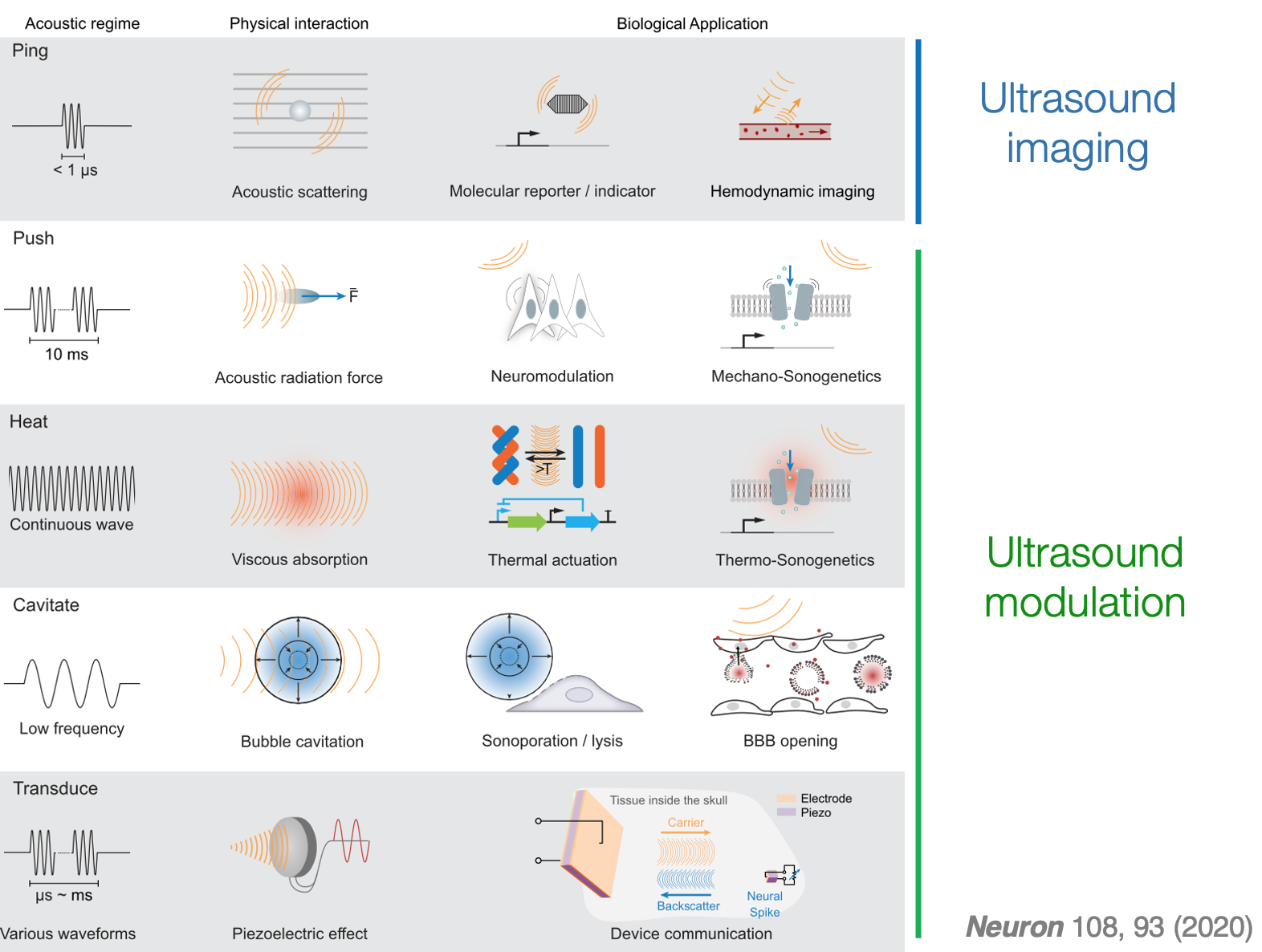

One modality that may bridge the gap between healthcare and consumer markets is ultrasound. It has shown promise in capturing neural activity through imaging hemodynamics, decoding movement intentions, and even expanding into areas like molecular imaging and neuromodulation. While hemodynamic imaging is already being used effectively, research is ongoing to develop molecular imaging techniques (similar to GCaMP, a genetically encoded calcium indicator) and smaller chronic devices for neuromodulation [7]. Ultrasound represents a good shot at building a neurotech platform as it could be used for various use cases (Chart 5).

Chart 5. Applications of ultrasound for imaging and modulation [7]

Some summit participants are working on the enabling technologies front. For instance, MintNeuro is aiming to bring semiconductor innovations to neurotech, focusing on improving miniaturisation and manufacturing processes to drive down costs. Additionally, Ucat is developing software for speech prosthetic devices with the goal of seamlessly integrating them into the larger virtual reality ecosystem.

The open-source approach is another crucial aspect that will contribute to the expansion of neurotech beyond the healthcare market. Open-source software (OSS) allows users to continue using a product even if its commercial developer ceases operations and allows enthusiasts to contribute to solving niche problems. While the summit did not extensively address the topic of open-source neurotech, its potential impact in fostering inclusivity and overcoming abandonment challenges cannot be overlooked.

In addition to horizontal/enabling technologies, OSS, and platforming, subsidising devices might be another strategy to lower costs for end users. Conor Russomanno mentioned using proceeds from expensive, say, $30,000 devices to subsidise simpler, $1,000 ones.

Despite some promising approaches to driving costs down and gaining a broader adoption, it remains uncertain whether medical neurotech companies will venture into consumer markets.

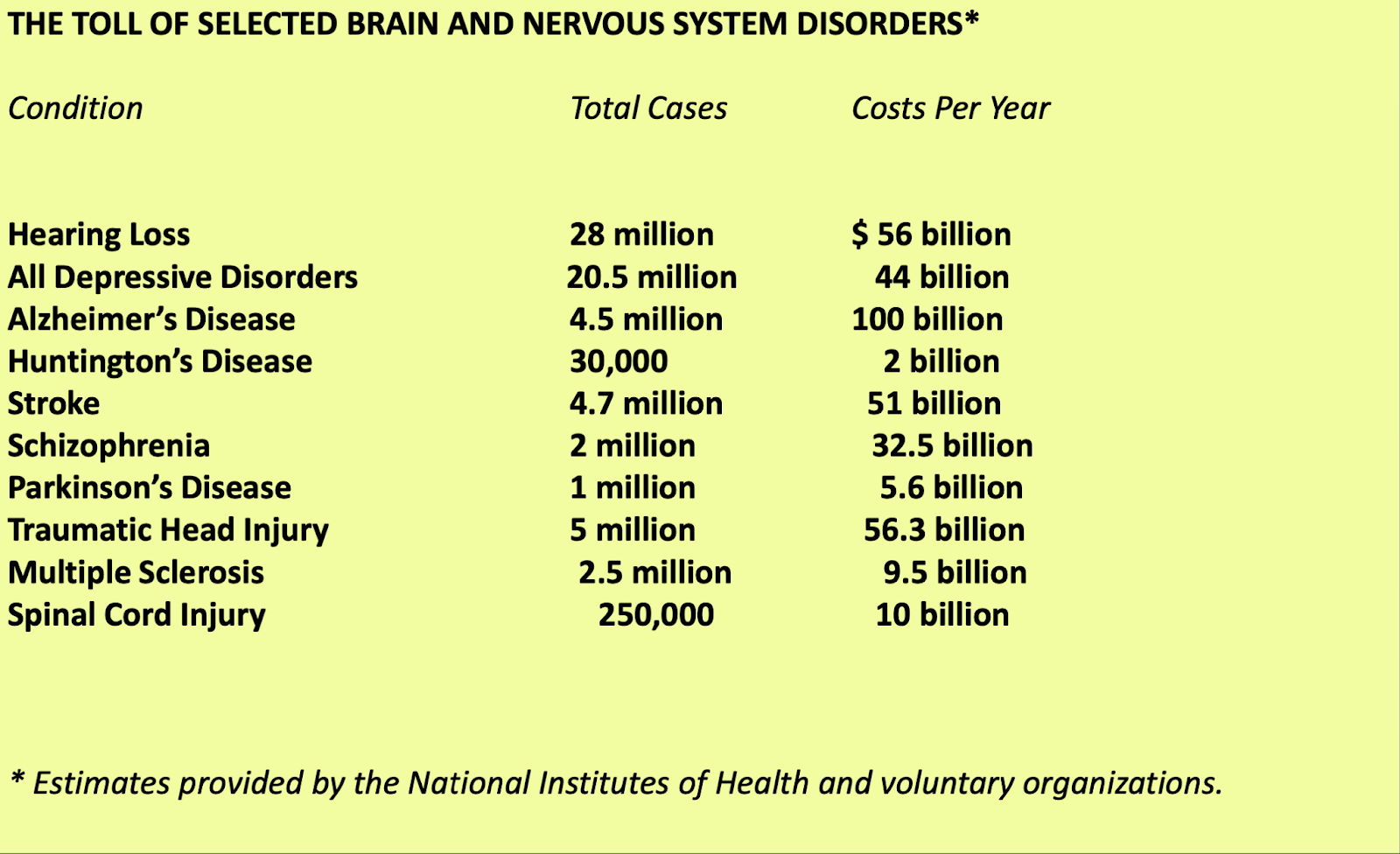

Medical neurotechnology markets typically cater to relatively small groups of patients, yet the financial implications per patient are significant. For instance, the annual cost attributed to each dementia case amounts to approximately $22,000 in the United States (Chart 6) and £32,000 in the UK. Although not every opportunity for cost savings might directly increase neurotech startups’ revenue, the potential financial benefit far surpasses that of traditional software companies. For example, Meta reported an average revenue of $39 per user by the end of 2022. This substantial difference underscores the financial incentives for companies to remain within the medical sector.

Chart 6 Selected brain and nervous system disorders [2]

It’s hard to tell what consumer applications will be the best match for medical neurotech or for building from scratch. Intuitively, I lean towards communication/social and productivity/memory-related use cases. A few exciting ideas were presented at the Summit.

Among other things, Damien Coyle [8] mentioned reconstructing three-dimensional hand movements based on data from a 32-channel EEG device and EEG applications for gaming. Penelope Lewis talked about sleep & memory enhancement. While talking about the healthcare applications, Tamar Malkin demonstrated an augmentation scenario of a prosthetic third thumb used by healthy users and suggested to ‘stay close to the body but not too close’ when developing neurotech. Among exhibitors, BrainPatch, Neudo, Neurocreate, and MyndPlay pitched consumer neurotech.

The summit undoubtedly left one with a sense of optimism about the future of neurotech. The astonishing technological advancements in the field hold immense potential.

Yet, the burning question isn't just about expanding the latest neurotech research into medical practice, but who'll steer this ship into uncharted consumer tech waters. Will the healthcare neurotech players, with their deep roots and visionary aspirations, take the helm, or will we see a new wave of consumer-centric disruptors echoing the seismic shift Apple triggered in the mobile industry? It's a thrilling possibility that both could coexist, merging the pioneering spirit of medtech with the game-changing audacity of consumer-first innovators, charting a course toward a future where technology and human experience intersect like never before.

To stay updated on the latest developments in neurotech, don't forget to subscribe here.

***

[1] Jörn Rickert, Presentation at the ‘Emerging and future applications of neural interfaces’ section of the Summit

[2] Andres Lozano, Presentation at the ‘Medical applications of neural interfaces’ section of the Summit

[3] Will Muirhead, Presentation at the ‘Emerging and future applications of neural interfaces’ section of the Summit

[4] Ioana Grigoras, Presentation at the ‘Medical applications of neural interfaces’ section of the Summit

[5] Victor Pikov, Presentation at the ‘Medical applications of neural interfaces’ section of the Summit

[6] Tim Denison, ‘Keynote address: Introduction to neural interface technologies’ at the Summit

[7] Mikhail Shapiro, Presentation at the ‘Emerging and future applications of neural interfaces’ section of the Summit

[8] Damien Coyle, Presentation at the ‘Non-medical applications of neural interfaces’ section of the Summit

[9] Conor Russomanno, Discussion ‘Designing inclusive devices’ at the Summit