How may PhD startup founders build for the long term?

This article was originally published in the Entrepreneur's Handbook publication on Medium, and scored 1K views (archived).

The current context supports research-heavy startups, there is even a special term for them — the ‘deep tech startup’ search query is reaching one peak after another on Google Trends. Investments in European deep tech grew from €0.7B in 2010 to €9.6B in 2019, according to Dealroom, an industry database.

Media attention and fresh capital, however, may lead to deep tech becoming a meme, rather than a useful concept. Something similar happened with artificial intelligence (AI) when every startup became an AI startup. Later, the research found no evidence that artificial intelligence was an important part of the products offered in 40% of 2,830 European AI.

Gil Dibner, the general partner at Angular Ventures noticed:

“… we live in an era where there are tremendous short-term benefits to successful pseudo entrepreneurship. In other words, you have a Ph.D. in computer science, you get your hands on a data set … — boom, a startup is born… And if you take a long view of their [founders] career, they’re missing out on the depth of things, experience, and authenticity of experience that I think informs the most interesting category-defining companies out there.”

In this article, I explore trends that underpin the deep tech concept, and how Ph.D. founders could build startups for the long term, based on these trends. I’m looking at the following trends and their interpretations:

- PhDs supply/academic demand encourages researchers to turn to entrepreneurship;

- Investing in Ph.D. founders — challenges with fundraising will likely remain;

- Cyclical nature of investing in doctoral founders, understanding these cycles is critical;

- Team composition of research-heavy startups starts to reflect the complexity of tech and science, its multidisciplinarity.

PhDs supply and demand

Entrepreneurship is becoming a more viable choice for Ph.D. founders. A reason for that is that other options are becoming less available. For example, the US continued to produce PhDs at an average annual rate of 2% between 1999 and 2019. American universities, however, decreased their reliance on full-time tenured or tenure-track staff, from 45% in 1975 to 29% in 2015. Joining a tech company or starting one’s own business becomes a more viable option as other alternatives disappear.

Tech itself becomes more complex and more appealing to research-minded founders. For instance, an increasing volume of genomics data coming out from large governmental projects creates an opportunity for biotech enthusiasts to launch startups. The availability of graphics processing units(GPUs) makes it possible to crunch this data.

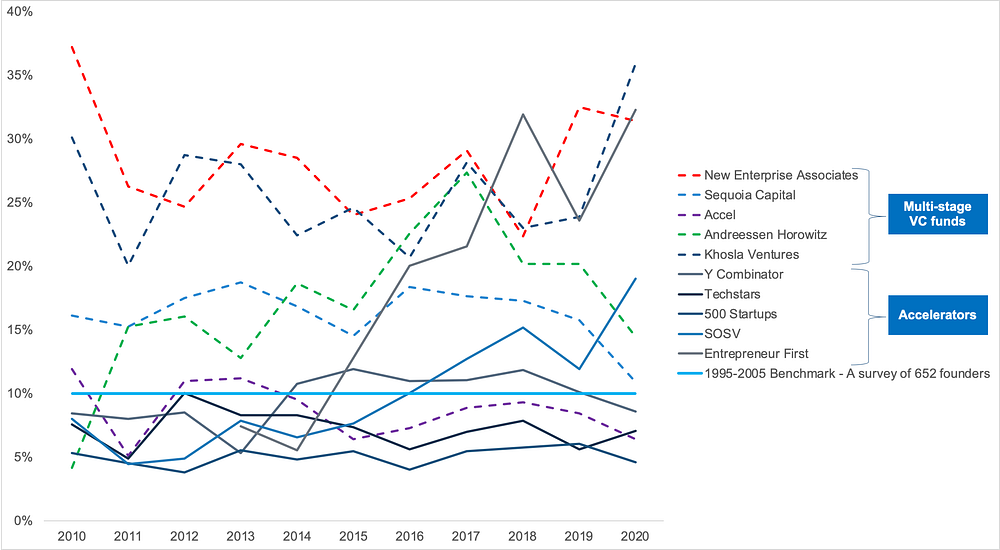

There is some evidence that more PhDs are turning their heads to startups.A survey of US-born founders of 502 engineering and technology companies, founded between 1995 and 2005, showed that only 10% of founders had a Ph.D. degree. However, the share of founders with doctoral degrees in portfolios of six out of ten leading investors keeps constantly higher than 10% during the recent decade (chart 1)*.

Chart 1. % of founders with a doctoral degree out of all founders associated with companies backed by selected investors annually

It also appears that when the right supporting infrastructure is in place, more PhDs start their own companies. For example, 14% of PhDs who participated in a Canadian not-for-profit industrial research partnerships programme in 2014–2015 started their own business. Given that only 19% of 2008/2010 doctoral graduates worked outside of research/education according to UK statistics, 14% of PhDs going into entrepreneurship looks impressive.

So what?

- I’d suggest PhDs to familiarise themselves with entrepreneurship earlier during their programmes, as the probability of embarking on this journey could be higher;

- Since more PhDs will join the startup land, finding a co-founder or hiring early employees among Ph.D. colleagues would become more common. To pick the best prospect, entrepreneurs need to hustle more.

Investment trends

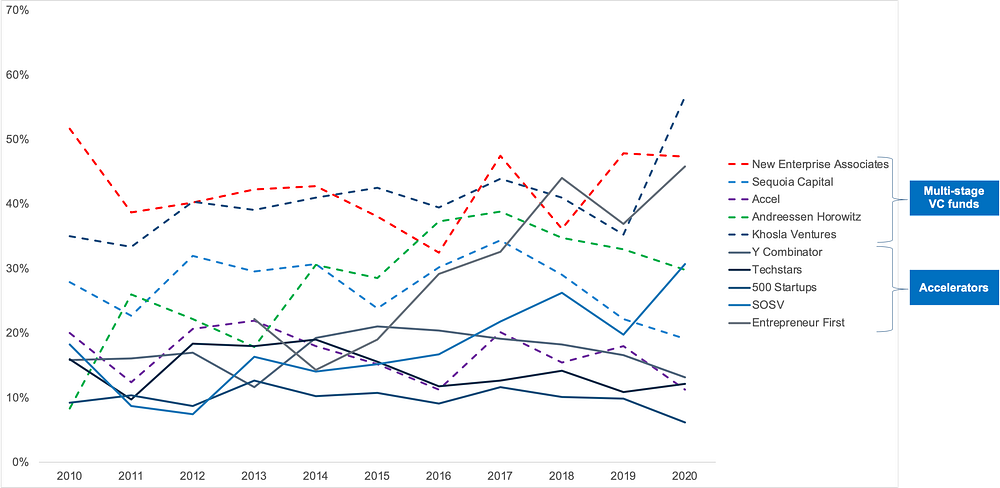

Surprisingly, the share of startups where at least one founder has a Ph.D. degree is not growing across portfolios of the leading investors. It rather fluctuates from year to year and does not form a clear trend (chart 2).

Chart 2. % of startups with at least one founder with a doctoral degree out of all startups backed by selected investors annually

We see some similar trends with investment volumes. Investments in European deep tech grew in absolute numbers, however during 2015–2020 it remained between 20–26% of all VC investments.

The influx of capital going into deep tech, therefore, may not be a result of strategic decisions and changes of investor preferences, but rather a result of “low-interest rates across the world [that] have pushed all investors into riskier asset classes”. What we may see is a rising tide that lifts all boats. The same tide sends these boats down.

The data also clearly shows investors’ preferences regarding founding research teams. For example, Entrepreneur First or Khosla Ventures may dedicate up to 46–57% of their annual deal activity to startups with at least one doctorate founder. Others, like Accel or Y Combinator, hardly go above 22%.

Moreover, there is a gap between early-stage generalist investors (accelerators) and their later-stage counterparts, who tend to invest in research-driven teams more frequently. The gap is addressed by early-stage specialist investors, the likes of Entrepreneur First where ‘…on average people with a technical Ph.D. are twice as likely to be offered a place [at a programme]’.

So what?

- Given that later-stage, VCs may have limited capacity to invest in deep tech, a challenge of going from ‘trying things out’ to building a business probably still persists.

Cyclicity of investing in research-heavy teams

The fact that the share of startups with at least one doctoral founder fluctuates year over year may suggest a cyclical nature of investing in Ph.D. founders (chart 2).

Ups and downs in investing in doctoral founders could be connected with the application/infrastructure cycles of a wider tech ecosystem. Sophia Yu from Tsingyuan Ventures points out ‘that deep tech will go through cycles that will sometimes favour PhD-founded companies, and will sometimes disfavour’. One of the possible conclusions from here could be that the deeper the industry cycle into infrastructure is, the more favourable it treats doctoral founders.

The cyclical nature of deep tech does not clearly stack with a belief that ‘…deep tech is the new tech’. Deep tech appears to be a sort of tech that flourishes, when an industry it is applied to comes through a certain phase of its development.

So what?

- It’s important to explore an industry that a Ph.D. founder wants to approach in order to spot the right ideas/research and the right point in time in order to transform these ideas into startups.

Multidisciplinarity and depth

Portfolios of ten selected investors to show that since 2010 the share of doctoral founders seems to be slightly increasing across founding teams with at least one doctoral founder. In 2020, eight out of ten funds had a ratio of doctoral founders at more than 50%, including three funds with a ratio above 60%, in their deep-tech portfolios (chart 3).

Chart 3. % of founders with doctoral degrees across portfolios of startups with at least one doctoral founder, backed annually by selected investors

Consequently, what we are seeing is not widespread of deep tech across portfolios of investors (nine out of ten still dedicate less than 50% of their deals to deep tech, chart 2), but an increasing complexity of research-heavy startups. Startups, which are already research-heavy, are becoming, even more, complex/deep, if measured by the share of doctoral founders.

Despite the fact that doctorate degree holders take up to 60% of a founding team in a research-heavy startup, there is still a place for a founder with another type of background. There is no visibility into the kinds of educational backgrounds of non-doctoral founders, however, one may expect something along the lines of a business/commercial background. Having looked at a much smaller sample of ten AI startups, I’ve found that six companies had a business/commercial founder in one way or another.

So what?

- More Ph.D. founders per startup, rather than more startups with at least one Ph.D. founder points to the increasing complexity, not the spread of deep tech. Founders need to be aware of associated challenges, e.g. the ’dual Ph.D. problem’.

- It is still important not to over-index on research, as the tech ecosystem matures, the importance of non-research factors will grow. Paul McNabb, a managing partner at Episode 1 Ventures noticed that:

“… five years ago really smart people with PhDs in machine learning or AI could get funded. The next stage was you needed to be those people, but you also need to have access to proprietary data to do your training. And now you need to have those two things. But you also need to have customer insight or access to real customer traction”.

Conclusion

A deep-tech concept is informed by various trends, including changes in supply/demand of PhDs, investors’ preferences, industry cycles, and increasing complexity of tech/science. Understanding these trends may help Ph.D. founders to avoid getting trapped by a meme, and to build for the long term.

***

✉️ ✉️ ✉️ For new writing subscribe on this website.

***

*Notes

Comparing portfolios of the leading investors may not be representative of the whole tech ecosystem, but it’s something one could track.

Data for charts 1,2, and 3 is from PitchBook, not from investors directly. For the count of the doctoral degrees, a keyword search of degree titles was used.

Annual investments include first-time investments, as well as follow-ons in portfolio companies backed earlier. Unique companies are counted, not deals. Companies may be counted multiple times if were backed by several investors from the list. Data is limited to companies with known founders who were with the company at the time of the transaction, as of 3/25/2021.

The most common doctoral degree is the Doctor of Philosophy (Ph.D.) — https://en.wikipedia.org/wiki/Doctorate.

In this article, the term ‘deep tech startup’ sometimes is used to label a startup where at least one founder has a doctoral degree.

Leading accelerators based on exits — https://www.forbes.com/sites/alejandrocremades/2018/08/07/top-10-startup-accelerators-based-on-successful-exits/ Entrepreneur First added to demonstrate an alternative ‘talent investing’ model.

Leading VC funds by the number of unicorns backed — https://www.cbinsights.com/research/best-venture-capital-unicorn-spotters-2/ only US investors selected.

***

Many thanks to Gil Dibner/Angular Ventures, Paul McNabb/Episode 1 Ventures, and Patrick Short/Sano Genetics for reviewing early drafts of this post and sharing ideas. Kudos to Mariette Clamens/PitchBook for helping with data crunching.